When Warren Buffett coined the term “economic moat”, he stated that the products that have wide, sustainable moats around them, are the ones that deliver rewards to investors.

That’s why determining the competitive advantage of any company is key to investing, to which moats were initially tethered: a bigger moat makes a stock a better bet.

But the implications are broader, for companies large and small. An effective moat doesn’t require Amazon’s distribution network or Microsoft’s monopolistic software strategy.

A moat-building project can be far simpler while still working toward the same goal: a sustainable, decisive business advantage.

Developing a moat isn’t formulaic. But companies with moats share common characteristics. This post will help you answer the question, “Which strategies are most likely to build a moat for my company?”

Table of contents

What is an economic moat?

An economic moat is a business which holds a long-term competitive advantage over the competition, which makes it difficult for competitors to reach their market share.

What’s the difference between a moat and a competitive advantage?

Moats are one type of competitive advantage. As Buffett suggests, they’re more durable than other competitive advantages.

Baseball offers an analogy. A mid-season trade for a player in the final year of a contract provides a short-term roster boost. It can give a team the third starter or extra bat they need to make a playoff run. But those players will leave at the end of the season.

A strong farm system, in contrast, takes longer to pay off. But it delivers year after year of new talent—talent that’s under contract for years to come. Mid-season trades are competitive advantages. Farm systems are moats.

Short-term advantages are useful, but they shouldn’t be mistaken for moat-building. There are two ways to build a moat:

- Dig a wide moat. Wide moats rely on several factors. For instance, Salesforce has a strong brand and exclusive integrations with Google Analytics 360. Sales reps are also likely to be familiar with Salesforce because it’s the most widely used CRM, reducing onboarding costs for companies that use it.

- Dig a deep moat. A deep moat is more difficult to overcome but isolated to a single characteristic. For example, in the United States, freight railroads have a deep moat. They own the tracks. An aspiring entrant would need to build a network of railways to compete independently.

Still, not everyone thinks moats are a good idea.

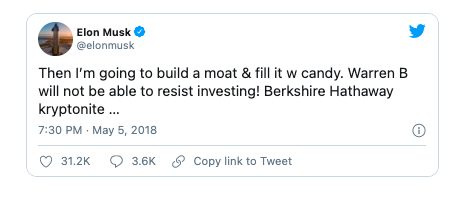

Warren Buffett, Elon Musk, and a fight over candy

Some years ago, before Elon Musk became part of Twitter’s history, Buffett and Musk got into a fight over candy.

The feud started when Musk was asked about Tesla’s decision to make its network of fast chargers accessible to other automakers (for a fee). Why would Tesla let others use its network, which could be a moat to protect it from electric competitors?

“I think moats are lame,” Musk responded. “It’s nice, sort of quaint, in a vestigial way. If your only defense against invading armies is a moat, you will not last long. What matters is the pace of innovation. That is the fundamental determinant of competitiveness.”

When told of Musk’s comment’s, Buffett acknowledged that technological change has made moats more vulnerable but not irrelevant. “Elon may turn things upside down in some areas,” but, Buffett suggested, “I don’t think he’d want to take us on in candy.”

Buffett’s company, Berkshire Hathaway, owns See’s Candies, and Buffett believes the company has a near-impenetrable moat, based mainly on its brand. Musk wasn’t impressed:

Posturing aside, there was a clear argument. Musk believes that moats are largely illusory—and also lazy. They stifle innovation. They may delay company death, but they also make that death inevitable.

You can build a moat that jealously guards an advantage without extending it. Or you can build one that gets deeper and wider as you innovate. To a large extent, it depends on the type of moat and how it’s deployed.

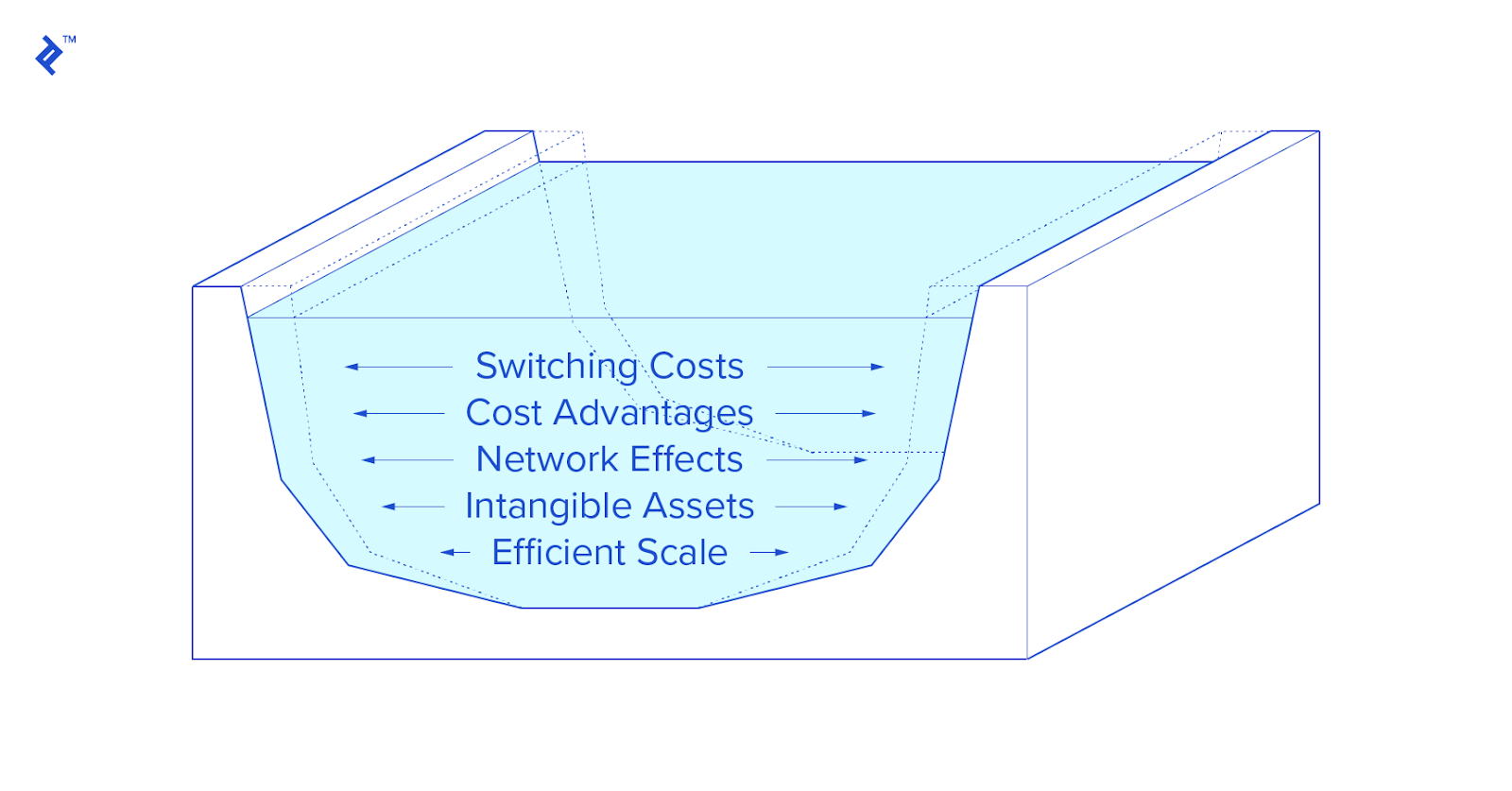

Five types of moats (and examples of each)

There are five types of moats:

- Low-cost production;

- High switching costs;

- Network effects;

- Intangible assets;

- Efficient scale.

Some moats have greater relevance (or irrelevance) for various industries.

1. Low-cost production

- Takeaway: If you’re in a commodity industry, be relentless when reducing costs—the lower you go, the deeper the moat.

If you can make it for less, you can sell it for less. Buffett, when thinking of low-cost production moats, uses GEICO (another Berkshire Hathaway acquisition) as an example. GEICO didn’t stumble upon low-cost production as its moat. It was essential for their market:

Most people will assume the service is fairly identical among [car insurance] companies, or close enough, so they’re going to do it on cost, so I gotta be the low-cost producer. That’s my moat. To the extent my costs get further lower than the other guy, I’ve thrown a couple of sharks into the moat.

When it comes to low-cost production, examples often focus on manufacturing and supply chain management. In Richard Rumelt’s Good Strategy Bad Strategy: The Difference and Why It Matters, he recounts a favorite (and recurring) discussion with his students: What makes Walmart successful? And why is it so difficult for others to compete?

Obviously, Walmart thrives as a low-cost producer. But how did it build that moat? The answer isn’t merely the reduced costs that come with scale, like buying in bulk. It is, Rumelt explains, the management of Walmart stores as a network.

The company limits costs through a management and distribution structure that serves multiple stores in a geographic area. The network of stores allows Walmart to limit its stock in any given store and share managerial expenses across the network. The moat is deep—efficiencies flow from a 5,000-store network.

2. High switching costs

- Takeaway: Customer data should improve the user experience, not make it tougher for people to leave.

More than any other moat, switching costs often serve companies, not consumers.

Until 2004, when the U.S. Federal Communications Commission rolled out Wireless Local Number Portability, cell phone service providers retained customers with high switching costs. If you left your provider, you lost your phone number. The moat offered nothing to consumers but made it easy for cell phone companies to keep clients around.

More recently, switching costs have centered on “data moats.” The decision to migrate a company Basecamp to Trello risks years of institutional knowledge. Leaving Gmail would cost you your list of contacts or historical messages. (You could export them, but there’s still a cost.)

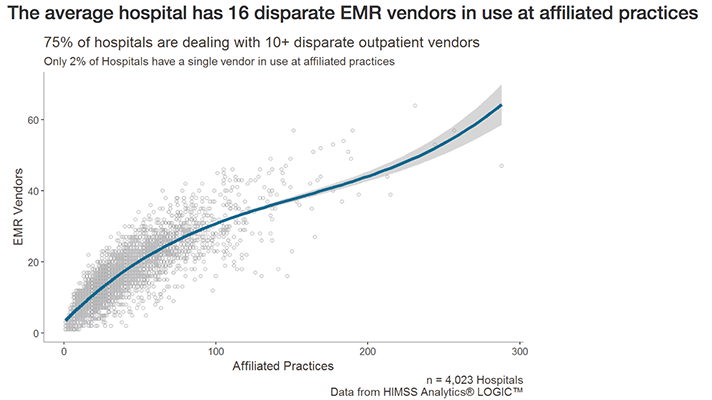

While email contacts transfer to other providers, interoperability isn’t common everywhere. Many companies actively thwart interoperability—its absence is their moat. This is especially true in health care, where electronic medical record (EMR) providers know that making their data play nice with other systems empowers customers to switch.

Given that the average hospital system uses 16 EMR providers, limiting interoperability protects an existing system and offers fertile ground for expansion. If an EMR provider rolls out a complementary product, its interoperability within their system makes it a tempting choice for current clients. This is the moat-building that Musk bemoans.

Social networks have their own switching costs. Twitter and Instagram are powerful platforms for personal brand building. Followers are non-transferable capital that users store on the platform. Leaving—or splitting time to pursue fans on a new network—comes at a cost.

That cost creates inertia that keeps users on an existing network and slows the growth of new ones. It’s the point of overlap between switching costs and network effects.

3. Network effects

- Takeaway: The positive impact of market share compounds—especially for software adoption.

Uber and eBay have something in common. Newcomers who take on either must answer the question, “Why bother with you if no one else is here?” Both companies built moats based on network effects. Their products become more valuable as they acquire users. (And competing products pale in comparison.)

A startup taxi service needs hundreds of drivers in a city before wait times can compete with Uber. The selection on eBay—of products (for buyers) or potential purchasers (for sellers)—took years to build.

A business model that requires a strong network effect is a long play. A slow, costly grind eventually hits a tipping point, when exponential growth finally delivers profitability.

The network effect is a powerful moat. It’s one that many venture capital–funded startups deploy. The primary goal is user acquisition. Profitability can be sorted out later, as was the case with WhatsApp.

WhatsApp focused on driving user adoption, and Facebook bought the company in 2014 without knowing how to monetize users. Zuckerberg felt that any platform with a half-billion users had potential, even if that required a $19 billion bet.

Zuckerberg paid, in other words, for the network-based moat: “WhatsApp is on a path to connect 1 billion people. The services that reach that milestone are all incredibly valuable.” (By 2019, WhatsApp had 1.5 billion users—but still no monetization. Uber isn’t profitable either.)

4. Intangible assets

- Takeaway: A strong brand may be the deepest moat that small companies can dig to fend off industry giants.

“Intangible assets constitute patents and trademarks,” writes Alex Graham, “but also hard-earned competitive advantages, such as brand names and culture.”

Some “intangible” assets are more defined than others. Patents and trademarks are legal lines. So are regulations, which, in some instances, are a cynical moat-digging campaign. TechCrunch’s Josh Constine challenged Facebook’s recent call for regulation as just such a ploy:

Young startups might be anchored by the weight of regulation. It could prevent them from ever rising to become a true alternative to Facebook. Venture capitalists choosing whether to fund the next Facebook killer might look at the regulations as too high of a price of entry.

Constine isn’t the only one with that opinion:

Musk, by making his fast chargers available to others and open-sourcing Tesla’s patents, has intentionally filled a potential moat. Doing so, in turn, has earned the company favorable publicity—publicity that digs an adjacent moat built on brand.

Compared to patents, brand is fragile. But it has no expiration date. Digging a brand moat is no different than building a brand. Buffett still laments Kodak’s decision, years ago, to allow Fuji to sponsor the Olympic Games:

Well, Kodak had that in spades, 30 years ago, they owned that. They had what I call share of mind [. . .] the little yellow box and everything—that said, “Kodak is the best.” That’s priceless.

They let Fuji come and start narrowing the moat in various ways. They let them get into the Olympics and take away that special aspect that only Kodak was fit to photograph the Olympics.

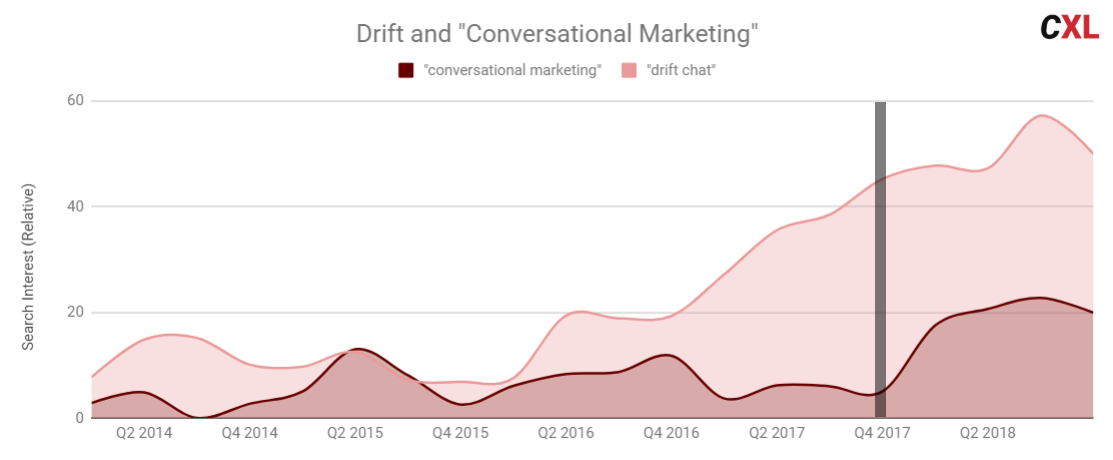

One way to dig a brand moat? Create a brand-owned term. HubSpot, which owns “inbound marketing,” has a brand moat, in part, because of its role defining the term. Even if other aspects of its brand diminish, it will always own the origin story of inbound marketing.

They’ve inspired imitators, such as Drift, which coined “conversational marketing” when it knowingly entered a commodity market. Given the choice between building a moat based on low-cost production or intangible assets, Drift chose brand. It’s worked out:

5. Efficient scale

- Takeaway: If demand has firm boundaries, aim for geographic dominance.

Moats built on efficient scale apply to a small number of businesses, like the aforementioned freight rail operators. They also apply to private companies that enjoy monopolies on public utilities, like electricity.

Efficient scale moats depend on limited demand and geographic dominance. For example, it’s financially feasible to build a competing motor speedway in Indianapolis. But demand won’t scale. The number of race fans or events won’t double with the availability of second track. However, if you took that project to a city without a raceway, the economics could work.

When geography is the determining factor, efficient scale relies on mergers and acquisitions. In the United States, the consolidation of health-care systems is a model for efficient scale moats: a rash of regional acquisitions.

The regional dominance of a single hospital system deters upstarts. Building a competing hospital in a market already served by a sprawling system won’t double procedures or ER admissions.

Because, in many cases, efficient scale moats were established decades ago, they’re the least relevant to modern businesses. Technological change, however, has created opportunities for new kinds of moats.

Moat-building in the 21st century

Technological innovation is a disrupter. It’s why Musk believes moats are irrelevant. But technology has also created new moats.

Inbound marketing

HubSpot’s Brian Halligan contends that Zappos’ moat doesn’t depend on its supply chain—a competitive advantage, perhaps, but a shallow moat at best. Instead, he argues, the company has built a digital moat:

The reason that we don’t start a company to compete with Zappos is not [its supply chain]. The moat around their business is the two million links into their website. How are we going to do that? It’s the 10 million Twitter followers they have, the massive number of Facebook likes. You can’t wake up overnight and get that.

Note: As of April 2019, Zappos had 2.5 million Twitter followers.

The crux of Halligan’s pitch is the value of inbound marketing. Inbound marketing may build a brand. But it also widens the moat in other ways, with hard-won backlinks and engaged social media followings.

The ability to reach large swaths of customers organically, via organic search, is a powerful moat. The increasing competitiveness in organic search and social media has deepened that moat for new entrants.

Within inbound marketing, there are parallels to Buffet’s more conservative approach and Musk’s free-for-all. Does a site link to other sites with “do follow” links? Is every attempt made to keep users from clicking elsewhere—even when external links serve user interest?

What is the guiding principle: fear or ambition?

Software adoption

Pick a random job description for a sales position. What are the odds that “knowledge of/experience with Salesforce” is on there? Software adoption—a moat of network effect—can protect a business from newcomers.

Common components of martech stacks become prerequisites (or, at least, preferred skill sets) for many positions, our current marketing operations role included:

Our current stack: Customer.io, Intercom, Hull.io, WordPress, Heap, Hubspot Sales, Mailshake, Clearbit, Unbounce, Google Analytics, Google Tag Manager, Metorik.

Software can be learned. It’s not the deepest moat. But a dominant position incentivizes practitioner learning, which, in turn, reinforces the software’s position in the market.

It’s an interesting argument in favor of a freemium version of a SaaS product. A freemium version could train thousands of users on your product, making it easier for companies with a paid version to find ready-to-work employees.

Similarly, widespread freemium adoption could motivate related software companies to develop integrations. Not surprisingly, the most popular products—freemium or not—earn early and powerful integrations. Those integrations can be lucrative, like Salesforce’s integration with Google Analytics 360.

Customer data

Facebook has built its moat with customer data. It’s done so primarily to benefit itself and, by extension, advertisers. Customer data doesn’t always work against the user.

For example, I’m reluctant to switch streaming music providers. Spotify’s recommendations are useful now that I’ve spent thousands of hours listening.

In other instances, consumers may not know that they benefit from use of their customer data. This is readily exemplified by segmentation and personalization. If your customer data allows you to deliver more relevant content, the customer has a better experience. And you reap the rewards of greater engagement.

Conclusion

To build moats—not just competitive advantages—every strategy needs to answer two questions:

- Does this effort build a sustainable, meaningful competitive advantage?

- Does that competitive advantage also benefit consumers?

A focus on moat-building is unlikely to inspire new strategies. But it does adjust the focus on which competitive advantages to pursue and adds urgency to the need to build multiple, sustainable advantages. It may mean, for example, devoting more ad spend to a brand campaign even if a sales-focused one might boost quarterly profits.

“Our managers of the businesses we run, I’ve got one message to them,” says Buffett, “which is to widen the moat. And we want to throw crocodiles and sharks and everything else, gators, I guess, into the moat to keep away competitors.”

Detractors, like Musk, ask pointed questions about the long-term costs of moat-building. Moats should serve consumer interests. They should encourage, not stifle, innovation. Technology has reshaped moats to be narrower and shallower.

No moat, however wide or deep, can protect a company from complacency.

Working on something related to this? Post a comment in the CXL community!

Related Posts

-

You invest in your employees—mentoring, conferences, training. Yet over time, unused knowledge fades. Employees take…

-

I recently had the pleasure of speaking with Nir Eyal, Stanford Business School lecturer, start…

-

How can you make Facebook Advertising work for B2B? I sat down with Curt Maly,…

-

Discover insider secrets on how to successfully build a high-performing growth team. How can you…

{kind=link}